In today's healthcare landscape, having a reliable insurance plan is more crucial than ever. Major medical insurance plans serve as the backbone of health coverage, providing essential protection against high medical costs. With a variety of options available, selecting the right plan can be overwhelming. This article aims to demystify major medical insurance plans, helping you make informed decisions regarding your health care needs.

Many individuals and families find themselves navigating the complex world of health insurance, often unsure of what major medical insurance plans entail. From understanding the benefits to learning about the different premiums, deductibles, and out-of-pocket costs, knowledge is power. By the end of this article, you will be equipped with the information needed to choose a plan that best suits your healthcare needs and financial situation.

As we delve deeper into the subject of major medical insurance plans, we will explore common questions, critical considerations, and essential features that these plans offer. Whether you're new to health insurance or looking to switch policies, this guide will serve as a valuable resource for understanding the ins and outs of major medical coverage.

What Are Major Medical Insurance Plans?

Major medical insurance plans are comprehensive health insurance policies designed to cover a significant portion of medical expenses. They typically cover a wide range of healthcare services, including hospital stays, surgeries, outpatient care, and preventive services. These plans are crucial for protecting individuals and families from the financial burden of unexpected medical emergencies.

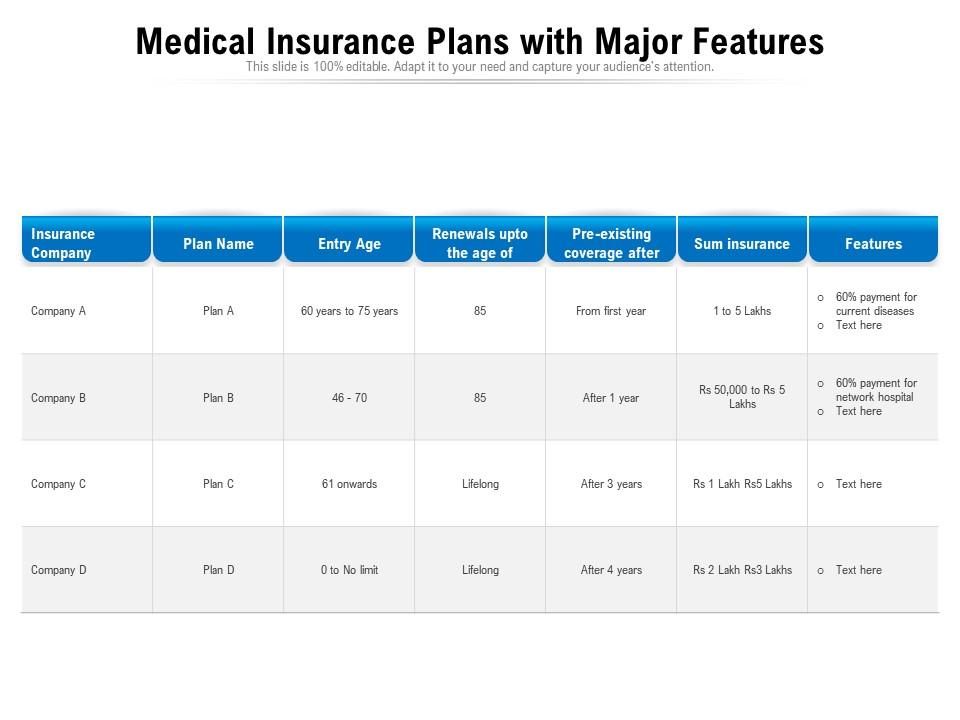

What Are the Key Features of Major Medical Insurance Plans?

- Coverage for Essential Health Benefits: Major medical plans cover essential health benefits mandated by law, including emergency services, hospitalization, maternity care, and mental health services.

- Preventive Services: Many plans offer coverage for preventive care at no additional cost, such as vaccinations and annual check-ups.

- Network of Providers: Most major medical plans operate within a network of healthcare providers, which can affect your out-of-pocket expenses.

- Out-of-Pocket Maximums: These plans usually feature an out-of-pocket maximum, limiting the total amount you may have to pay for covered services in a plan year.

How Do Major Medical Insurance Plans Work?

Major medical insurance plans function by sharing the costs of healthcare between the insured and the insurance provider. When you receive care, you may need to pay a deductible, which is the amount you must pay before your insurance begins to cover costs. After meeting your deductible, you typically pay a copayment or coinsurance for services, while the insurance covers the remaining expenses.

What Are the Different Types of Major Medical Insurance Plans?

Major medical insurance plans can be categorized into several types, each with unique features and advantages. Understanding these types can help you determine which plan best fits your needs:

- Health Maintenance Organization (HMO): Requires members to choose a primary care physician and get referrals for specialist care.

- Preferred Provider Organization (PPO): Offers more flexibility in choosing healthcare providers and does not require referrals.

- Exclusive Provider Organization (EPO): Similar to PPOs but does not cover out-of-network services, except in emergencies.

- Point of Service (POS): Combines features of HMO and PPO plans, allowing members to choose between in-network and out-of-network care.

How to Choose the Right Major Medical Insurance Plan?

Choosing the right major medical insurance plan involves evaluating several factors:

- Coverage Needs: Assess your healthcare needs, including any chronic conditions, medications, and anticipated medical services.

- Budget: Consider your budget for premiums, deductibles, and out-of-pocket expenses.

- Provider Network: Verify if your preferred doctors and hospitals are included in the plan’s network.

- Plan Ratings: Research customer reviews and ratings for the insurance provider to ensure quality service.

What Are the Costs Associated with Major Medical Insurance Plans?

The costs of major medical insurance plans can vary significantly based on factors such as age, location, and the type of plan you choose. Key cost components include:

- Premiums: The monthly payment required to keep your insurance active.

- Deductibles: The amount you pay out-of-pocket before your insurance begins to cover costs.

- Copayments: Fixed fees for specific services, such as doctor visits or prescriptions.

- Coinsurance: The percentage of costs you share with your insurance after meeting your deductible.

What Should You Consider Before Enrolling in a Major Medical Insurance Plan?

Before enrolling in a major medical insurance plan, consider the following:

- Examine Coverage Terms: Read the fine print to understand what is covered and what is not.

- Check for Exclusions: Be aware of any services that may not be covered by the plan.

- Evaluate Customer Service: Research the insurance provider’s customer support options and responsiveness.

- Look for Additional Benefits: Some plans may offer wellness programs, telehealth services, or discounts on fitness memberships.

Conclusion: Are Major Medical Insurance Plans Right for You?

Major medical insurance plans are essential for protecting yourself and your family from the high costs of healthcare. By understanding the features, types, and costs associated with these plans, you can make informed decisions that align with your healthcare needs and financial situation. Whether you are exploring your options for the first time or considering a change, the right major medical insurance plan can provide peace of mind and security in times of medical need.