Hard inquiries can have a significant impact on your credit score, making it essential to know how to remove them effectively. When you apply for credit, lenders perform hard inquiries to assess your creditworthiness, which can temporarily lower your score. Understanding how to navigate this process can help you maintain a healthy credit profile. In this article, we will explore the steps you can take to remove hard inquiries from your credit report, the importance of monitoring your credit, and how to protect your financial future.

Hard inquiries, also known as hard pulls, occur when a lender checks your credit for lending purposes. Unlike soft inquiries, which do not affect your credit score, hard inquiries can stay on your credit report for up to two years. This article will provide you with a comprehensive guide on how to remove hard inquiries, the implications of these inquiries on your credit score, and tips on maintaining good credit health.

By following the strategies outlined in this guide, you can take control of your credit report and improve your financial standing. Whether you're preparing for a major purchase or just want to ensure your credit is in good shape, understanding how to manage hard inquiries is crucial. Let's dive into the details!

Table of Contents

- What Are Hard Inquiries?

- How Hard Inquiries Affect Your Credit Score

- How to Check for Hard Inquiries

- Steps to Remove Hard Inquiries

- Disputing Hard Inquiries

- Preventing Future Hard Inquiries

- Monitoring Your Credit Report

- Conclusion

What Are Hard Inquiries?

Hard inquiries occur when a lender or financial institution checks your credit report as part of their decision-making process for lending. Unlike soft inquiries, which include checks made by you or companies for promotional purposes, hard inquiries can impact your credit score. Here are some key points about hard inquiries:

- They are recorded when you apply for new credit, such as loans, credit cards, or mortgages.

- Hard inquiries can remain on your credit report for up to two years.

- Multiple inquiries in a short period can signal to lenders that you are experiencing financial distress.

How Hard Inquiries Affect Your Credit Score

Understanding how hard inquiries affect your credit score is essential for maintaining good credit health. Here are some important aspects to consider:

- Each hard inquiry can lower your credit score by a few points, usually between 5 to 10 points.

- Too many hard inquiries in a short time frame can have a more significant negative impact.

- Hard inquiries account for about 10% of your overall credit score.

How to Check for Hard Inquiries

To effectively manage hard inquiries, you need to know how to check your credit report. Follow these steps:

- Request a free credit report from each of the three major credit bureaus: Equifax, Experian, and TransUnion at AnnualCreditReport.com.

- Review your credit report for any hard inquiries that you do not recognize.

- Take note of the dates and the institutions that performed the inquiries.

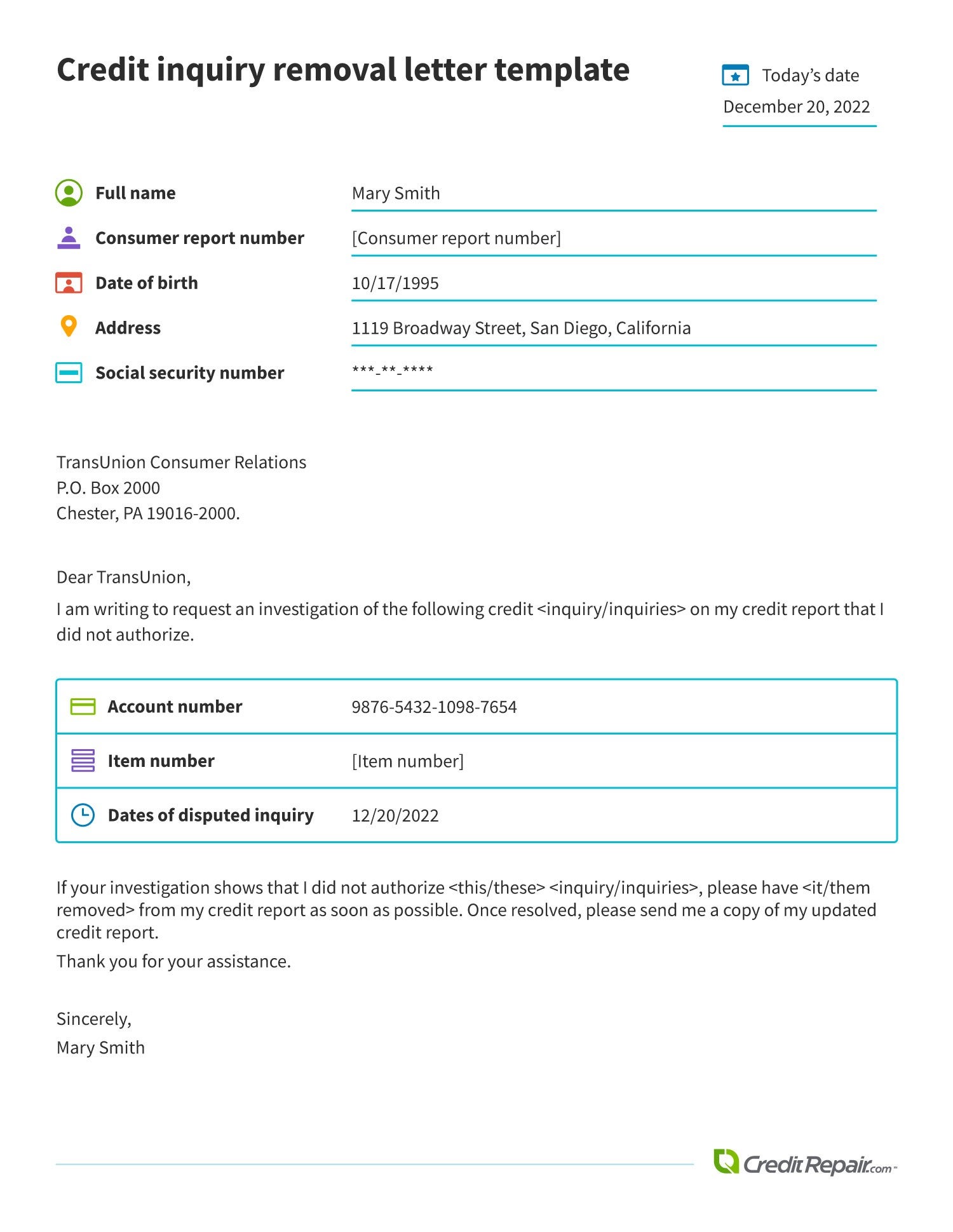

Steps to Remove Hard Inquiries

If you find hard inquiries on your credit report that you believe are inaccurate or unauthorized, follow these steps to remove them:

- Gather documentation: Collect any records that support your claim that the inquiry is incorrect.

- Contact the creditor: Reach out to the lender that made the inquiry and ask them to remove it.

- File a dispute with credit bureaus: If the creditor does not cooperate, file a dispute with the credit bureaus that reported the inquiry.

Disputing Hard Inquiries

Disputing a hard inquiry requires a systematic approach. Here’s how to do it:

- Write a dispute letter: Clearly state your reasons for disputing the inquiry and include any supporting documentation.

- Send the letter: Mail your dispute letter to the credit bureau(s) reporting the inquiry.

- Wait for a response: The credit bureau typically has 30 days to investigate and respond to your dispute.

Preventing Future Hard Inquiries

To avoid future hard inquiries, consider these preventative measures:

- Limit applications for new credit: Only apply for credit when necessary.

- Research lenders: Compare lending options before submitting applications to minimize hard inquiries.

- Use prequalification tools: Many lenders offer prequalification options that do not result in hard inquiries.

Monitoring Your Credit Report

Regularly monitoring your credit report can help you stay on top of hard inquiries and maintain a good credit score. Here are some tips:

- Use credit monitoring services: Consider signing up for a credit monitoring service that alerts you to changes in your credit report.

- Review your credit report regularly: Check your reports at least once a year to ensure accuracy.

- Stay informed about credit score factors: Understanding what affects your credit score can help you make better financial decisions.

Conclusion

In summary, managing hard inquiries is crucial for maintaining a healthy credit profile. By understanding what hard inquiries are, how they affect your credit score, and the steps to remove them, you can take control of your financial future. Don’t hesitate to monitor your credit regularly and dispute any inaccuracies you find. If you have any questions or experiences to share regarding hard inquiries, please feel free to leave a comment below. Remember to share this article with anyone who could benefit from this information and explore our other resources for more tips on improving your credit health.

Sources: